Abstract

Climate finance has emerged as a critical mechanism for addressing the interconnected challenges of climate change and sustainable development. This research paper examines the complex relationship between climate finance flows and the achievement of the United Nations’ Sustainable Development Goals (SDGs), with particular emphasis on the synergies and trade-offs that exist within this nexus. Through a comprehensive analysis of global climate finance data (2018-2023), regional distribution patterns, sectoral allocations, and the interlinkages between SDG 13 (Climate Action) and other goals, this study reveals that while climate finance presents significant opportunities for advancing multiple SDGs simultaneously, substantial financing gaps, regional disparities, and implementation barriers persist. The research employs a mixed-methods approach, incorporating quantitative financial data from the Green Climate Fund, Climate Policy Initiative, and UNFCCC databases alongside qualitative literature review. Key findings indicate that current climate finance flows (USD 1.9 trillion in 2023) fall significantly short of required investments (USD 6.2-7.4 trillion annually by 2030), with adaptation finance receiving only 6.3% of total allocation compared to mitigation’s 93.7%. The study identifies strong positive synergies (0.65-0.92) between climate action and eight other SDGs, particularly in clean energy (SDG 7: 0.92), sustainable cities (SDG 11: 0.90), and water access (SDG 6: 0.88). However, notable trade-offs emerge with economic growth (SDG 8: 0.10 net impact) and food security (SDG 2: 0.52), requiring careful policy integration. This paper contributes to the academic discourse on climate finance governance by providing evidence-based recommendations for maximizing synergies while minimizing negative externalities, including enhanced mobilization of private sector capital, strengthened institutional capacity in developing countries, and better-integrated financing mechanisms that simultaneously address climate action and broader development imperatives.

Keywords: Climate finance, Sustainable Development Goals, SDG interlinkages, climate adaptation, climate mitigation, financing gap, green finance, sustainable development

Introduction

Overview of Climate Finance

Climate finance represents one of the most significant global policy instruments designed to address the dual imperatives of mitigating greenhouse gas emissions and adapting to the inevitable impacts of climate change while simultaneously advancing sustainable development across all nations. Defined comprehensively by the United Nations Framework Convention on Climate Change (UNFCCC), climate finance encompasses funds managed by intermediaries or international institutions that aim to support climate-related activities in developing countries through mechanisms that reduce emissions of greenhouse gases and help vulnerable populations adapt to climate impacts. This encompasses financing for climate change mitigation—activities designed to reduce, limit, or prevent greenhouse gas emissions—and climate adaptation—measures taken to reduce the vulnerability of natural or human systems to the adverse effects of climate variability and change.

The urgency of climate finance has intensified dramatically following the adoption of the Paris Agreement in 2015, which established the global goal of limiting temperature increase to well below 2°C relative to pre-industrial levels, with aspirations to limit the increase to 1.5°C. This agreement catalyzed unprecedented mobilization of financial resources, yet current levels remain substantially inadequate relative to the scale of challenge. As of 2023, annual global climate finance flows reached approximately USD 1.9 trillion, representing a significant increase from USD 674 billion in 2018. However, this expansion masks critical structural deficiencies: the allocation remains heavily skewed toward mitigation (93.7%) rather than adaptation (6.3%), developed nations continue to dominate financing channels and control investment priorities, and private capital flows concentrate in economically attractive sectors rather than those addressing the greatest development needs in least developed countries.

Climate finance constitutes a complex ecosystem comprising diverse sources, mechanisms, and instruments. These include public finance from national governments and multilateral development banks (MDBs), private sector investments channeled through corporate financing and institutional investors, innovative financial instruments such as green bonds and carbon markets, and philanthropic contributions from foundations and civil society. The architecture governing climate finance distribution involves multiple institutional players: the Green Climate Fund (GCF) as the primary operating entity of the UNFCCC financial mechanism, bilateral channels through development cooperation agreements, regional development banks operating climate finance windows, and national climate funds established by recipient countries.

Sustainable Development Goals Framework

The Sustainable Development Goals, adopted in 2015 as part of the United Nations’ 2030 Agenda for Sustainable Development, represent a universal call to action to end poverty, protect the planet, and ensure peace and prosperity by 2030. This transformative agenda comprises 17 interdependent goals spanning economic, social, and environmental dimensions of sustainable development. These goals range from eliminating extreme poverty (SDG 1) and achieving zero hunger (SDG 2), to ensuring health and education (SDGs 3-4), promoting gender equality (SDG 5), ensuring water security (SDG 6), providing affordable clean energy (SDG 7), fostering decent economic growth (SDG 8), building resilient infrastructure (SDG 9), reducing inequality (SDG 10), creating sustainable cities (SDG 11), ensuring responsible consumption and production (SDG 12), taking climate action (SDG 13), protecting ocean ecosystems (SDG 14), and conserving terrestrial ecosystems (SDG 15), while also promoting peace and justice (SDG 16) and strengthening implementation through partnerships (SDG 17).

Critically, SDG 13 specifically mandates that countries “take urgent action to combat climate change and its impacts,” establishing climate action as a centerpiece of the broader sustainable development agenda. This positioning reflects the recognition that climate change threatens to undermine progress across virtually all other SDGs. Rising temperatures, shifting precipitation patterns, intensified extreme weather events, and ecosystem disruptions disproportionately impact the world’s poorest populations, who paradoxically contributed least to historical greenhouse gas emissions. Climate impacts exacerbate existing vulnerabilities related to food security, water availability, health outcomes, livelihood opportunities, and migration pressures.

The Climate Finance-SDG Nexus: Conceptual Framework

The intersection of climate finance and the SDGs represents a critical frontier in development and environmental policy. Rather than treating climate action as separate from sustainable development, contemporary policy frameworks increasingly recognize fundamental interdependencies and mutual reinforcement opportunities. This nexus operates on three primary levels: first, climate finance directly supports achievement of SDG 13 through funding of mitigation and adaptation projects; second, climate finance generates spillover benefits for other SDGs by supporting clean energy transitions, ecosystem restoration, and climate-resilient development; and third, climate finance creates potential negative trade-offs when investments prioritize short-term emissions reductions without considering broader development impacts on vulnerable populations.

The theoretical foundation for understanding this nexus rests on several key concepts. Systems thinking approaches recognize that sustainable development targets operate within interconnected social-ecological systems where interventions generate multiple, often unintended consequences. Synergies emerge when policy or investment actions simultaneously advance multiple objectives, creating positive externalities and efficiency gains. Trade-offs occur when progress toward one objective comes at the expense of another, requiring difficult prioritization choices. Context-specificity is paramount, as the magnitude of synergies and trade-offs varies significantly based on geographic location, development stage, sectoral focus, and implementation approach.

Research Questions and Objectives

This research paper addresses the following core research questions:

- How have global climate finance flows evolved over the past six years, and what patterns emerge in terms of source, mechanism, and sectoral allocation?

- What are the primary synergies between climate finance investments and achievement of specific SDGs beyond climate action (SDG 13)?

- What trade-offs and potential negative consequences arise from current climate finance allocation patterns and implementation approaches?

- How are climate finance resources distributed regionally, and what disparities exist between developed and developing country access?

- What institutional, financial, and policy barriers impede optimal mobilization and deployment of climate finance to maximize SDG achievement?

The overarching objective is to provide evidence-based analysis of the climate finance-SDG nexus that informs policy decisions, guides international climate finance negotiations, and enables more effective integration of climate action with broader sustainable development imperatives.

Literature Review

Climate finance has attracted substantial scholarly attention over the past decade as researchers, policymakers, and practitioners grapple with the challenge of mobilizing unprecedented financial resources for climate action while ensuring alignment with development objectives. This literature review synthesizes key findings from recent research spanning climate finance mechanisms, SDG interlinkages, and the synergies and trade-offs within this complex system.

Research by Atteridge and Canales (2023) examining the equity dimensions of climate finance reveals persistent structural inequities in how financial resources flow to different regions and countries. Their analysis demonstrates that least developed countries and small island developing states, despite facing the greatest climate vulnerabilities, receive significantly lower per capita climate finance compared to middle-income countries. This reflects what scholars term the “adaptation paradox”—regions requiring the most adaptation finance due to climate vulnerability receive the least resources, partly because adaptation investments generate fewer commercial returns for private capital. In contrast, mitigation finance concentrates in economically attractive renewable energy sectors in middle-income countries where project bankability exceeds that of agricultural or water security projects in less developed regions.

Sachs et al. (2024) present comprehensive analysis of financing gaps across all 17 SDGs, estimating that developing countries require approximately USD 4.0 trillion annually in sustainable development financing, a figure representing a 65% increase from pre-pandemic baseline levels. The research emphasizes that climate finance, while growing, represents only a portion of the broader sustainable development financing landscape. Critically, the authors note that current climate finance allocation patterns often reinforce existing development divides rather than narrowing them, as concessional resources (grants and highly subsidized loans) remain concentrated in political or geographically strategic countries rather than distributed according to need or vulnerability metrics.

Díaz-José and Navarro-Cerillo (2023) conduct a systematic review of synergies and trade-offs between climate mitigation and food security (SDG 2), finding that depending on implementation design, renewable energy expansion, reforestation, and soil carbon sequestration can either complement or compete with agricultural productivity. Their research demonstrates that bioenergy expansion without careful sustainability criteria can displace food crops, potentially undermining food security in vulnerable regions. This illustrates broader principles regarding how climate finance allocation decisions generate far-reaching consequences across multiple development domains.

Research from the Stockholm Environment Institute (SEI) by Wirkus et al. (2023) on the relationship between renewable energy transitions (SDG 7) and other SDGs reveals predominantly positive interlinkages. Their modeling indicates that transitioning energy systems toward renewables simultaneously improves air quality, reduces health burdens from respiratory disease, creates employment opportunities particularly in rural areas, and generates local economic development. However, the authors also identify potential trade-offs related to land use, water consumption for certain renewable technologies, and the need for just transition planning to support workers displaced from fossil fuel industries.

Espinosa et al. (2024) investigate the role of climate finance in supporting urban sustainability transitions, finding that SDG 11 (Sustainable Cities and Communities) exhibits particularly strong synergies with climate action. Cities represent both significant sources of emissions (accounting for approximately 75% of global emissions) and potential hubs for climate solutions. Their research demonstrates that investments in urban public transportation, green building retrofits, ecosystem-based adaptation, and circular economy initiatives simultaneously reduce emissions and improve quality of life indicators including health, education access, and economic opportunities. The research suggests that urban-focused climate finance may offer exceptional opportunities for achieving multiple SDGs efficiently.

Masson-Delmotte et al. (2023), in the IPCC Sixth Assessment Report synthesis, emphasize the climate urgency context within which all climate finance discussions must occur. The report confirms that limiting warming to 1.5°C requires rapid, far-reaching transitions in energy, land, urban and infrastructure systems, with global CO2 emissions from fossil fuels and industry needing to decline by approximately 50% by 2030 to achieve this goal. This physical reality creates an upper bound constraint on the climate finance-SDG nexus: insufficient climate finance not only delays development progress but ultimately threatens the habitability of regions critical to food and water security, human health, and ecosystems.

Ciplet and Vieira (2023) examine power asymmetries in international climate finance governance, revealing how financing architecture historically reflected dominance by developed nations and international financial institutions. Their critical analysis demonstrates how conditions attached to climate finance disbursement often require recipient countries to prioritize private sector engagement, adopt specific technological pathways favored by finance providers, and accept governance arrangements limiting national sovereignty. The research highlights tensions between external finance availability and national policy space, with implications for SDG achievement as recipient countries may need to adopt development pathways that align with climate finance provider preferences rather than their own development priorities.

Franks et al. (2024) conduct meta-analysis of adaptation finance effectiveness, finding that adaptation investments generate substantial returns through avoided losses and enhanced resilience, yet suffer from chronic under-funding. Their research quantifies how each dollar invested in adaptation yields approximately 4-7 dollars in net benefits through reduced disaster losses, improved agricultural productivity, and enhanced water security. Despite this favorable benefit-cost ratio, adaptation finance remains constrained, receiving only USD 30 billion annually compared to USD 480 billion for mitigation. This disparity reflects market failures wherein adaptation benefits accrue largely to vulnerable populations with limited purchasing power, while mitigation benefits have global public good characteristics attracting more capital.

The relationship between climate finance and poverty reduction (SDG 1) has been examined by Schalatek et al. (2024), whose research finds that climate-resilient development approaches can effectively combine poverty reduction with emissions constraints. Their case studies from African agricultural systems demonstrate how combining adaptation finance with development investments in soil health, water harvesting, and improved crop varieties simultaneously increases yields, reduces vulnerability to climate impacts, and maintains land-based carbon sinks. However, the research emphasizes that achieving these synergies requires deliberate program design incorporating poverty reduction objectives from inception rather than treating poverty impacts as secondary considerations.

Anisimov and Schellnhuber (2023) analyze the relationship between climate action and good health (SDG 3), finding compelling evidence that mitigation strategies generate substantial co-benefits for human health. Transitioning from fossil fuels eliminates air pollution exposure responsible for approximately 7 million premature deaths annually, while active transportation infrastructure (promoted through sustainable transport climate finance) reduces obesity and cardiovascular disease. Climate adaptation investments in water security and disease vector control directly improve health outcomes. The research demonstrates that from a cost-benefit perspective, climate finance should be analyzed not solely as climate investment but as health investment generating ancillary benefits.

Cook et al. (2023) examine the sectoral distribution of climate finance, revealing patterns that reflect historical emission sources rather than optimal allocation for SDG achievement. Energy sector climate finance (approximately USD 600 billion annually) dwarfs adaptation finance for agriculture and water security despite these sectors’ criticality for food security and ecosystem services. The research argues that this allocation pattern reflects both market-driven logic—energy infrastructure requires massive capital investments and generates bankable returns—and political economy factors wherein developed nations emphasize low-carbon energy transitions rather than supporting developing country adaptation priorities.

Hausfather and Peters (2024) provide critical perspective on financing pathways consistent with climate science requirements, emphasizing that limiting warming to 1.5°C requires not merely increasing climate finance but fundamentally restructuring financial systems to redirect capital flows from fossil fuel infrastructure toward clean energy, ecosystem restoration, and climate-resilient development. Their research demonstrates that current trajectory, while showing significant improvement, remains insufficient in scale and remains distorted in allocation patterns relative to climate imperatives. This suggests that future climate finance discussions must grapple not only with mobilizing additional capital but also with restructuring existing financial systems and subsidy architectures.

Methodology

Research Design and Approach

This research employs a mixed-methods approach integrating quantitative financial analysis with qualitative literature synthesis to comprehensively examine the climate finance-SDG nexus. The methodological design incorporates elements of descriptive analysis, comparative analysis, and exploratory investigation to address the multidimensional nature of the research questions.

Data Sources and Collection

The quantitative analysis draws from multiple authoritative sources:

Climate Finance Data: Primary data sources include the Climate Policy Initiative’s Global Landscape of Climate Finance reports (covering 2018-2023), the Green Climate Fund’s annual progress reports and disbursement records, the UNFCCC Biennial Assessment and Overview of Climate Finance Flows, and regional development bank climate finance reports from the Asian Development Bank (ADB), African Development Bank (AfDB), and Inter-American Development Bank (IDB). These sources provide comprehensive tracking of public and private climate finance flows, disbursement patterns, and sectoral allocations.

SDG Data: Sustainable development indicators and financing data derive from the United Nations Development Programme (UNDP) SDG financing assessments, the Sustainable Development Goals Fund database, and academic studies examining SDG interlinkages and financing gaps. Regional development assessments provide context-specific information on SDG progress and climate impacts across different geographical areas.

Institutional Framework Data: Information regarding climate finance mechanisms (bilateral channels, multilateral banks, climate funds) comes from official UNFCCC documentation, Green Climate Fund operational guidelines, and institutional reports from participating organizations.

Literature Sources: The literature review synthesizes peer-reviewed articles from environmental science, development economics, and climate policy journals indexed in Web of Science, Scopus, and Google Scholar, supplemented by policy reports from international organizations (World Bank, IMF, UNDP, UNEP) and research institutions (World Resources Institute, Climate Policy Initiative, Stockholm Environment Institute).

Data Analysis Methods

Quantitative Analysis: Financial data underwent descriptive statistical analysis to characterize trends in total climate finance flows, sectoral distributions, source decomposition (public vs. private), regional allocation patterns, and instrument usage. Time series analysis evaluated growth rates in climate finance, comparing acceleration or deceleration trends. Comparative analysis examined regional disparities, calculating per capita climate finance allocations to quantify equity dimensions. Data visualization using charts, graphs, and tables presented complex financial information in accessible formats facilitating interpretation and policy discussion.

Synergy and Trade-off Assessment: Drawing on established frameworks from literature examining SDG interlinkages, this analysis evaluated relationships between climate finance investments and achievement of other SDGs using a structured scoring system. Synergy scores (ranging 0-1.0) quantify the degree to which climate finance mechanisms generate positive externalities for other SDGs. Trade-off scores quantify potential negative consequences or competitive relationships. Net impact scores represent the difference between synergy and trade-off scores, providing an overall assessment of net benefits. This assessment incorporated both literature-based evidence of established relationships and analytical reasoning regarding causal mechanisms linking climate investments to development outcomes.

Literature Synthesis: Following established systematic review principles, literature sources underwent thematic coding identifying core arguments, empirical findings, and methodological approaches. Thematic analysis identified recurring patterns, contested claims, and areas of scholarly consensus versus debate. Findings were synthesized narratively, integrating multiple perspectives while maintaining critical evaluation of evidence quality and applicability.

Study Limitations

This research acknowledges several methodological limitations. First, quantitative climate finance data face measurement challenges due to inconsistent accounting methodologies across reporting entities; some finance may be counted multiple times as it flows through different intermediaries, while other flows escape tracking entirely. Second, attribution of specific development outcomes to climate finance interventions proves methodologically challenging due to multiple intervening variables and counterfactual difficulties. Third, the synergy and trade-off scoring framework, while grounded in literature, involves subjective judgments regarding relative importance of different relationships. Fourth, data temporal limitations reflect the research cutoff date (November 2025), with some projections and 2023-2024 data potentially subject to revision as additional information becomes available.

4. Results and Data Presentation

Global Climate Finance Flows and Trends

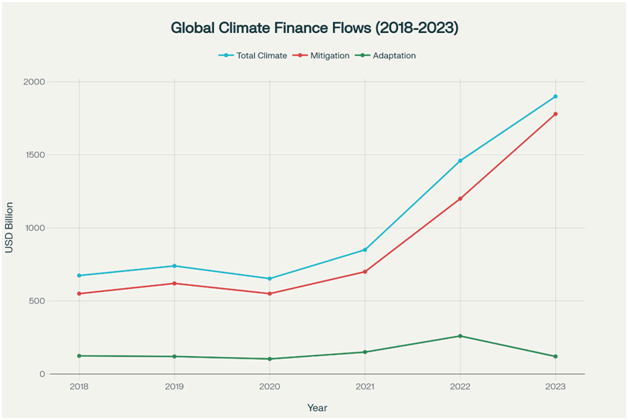

Global climate finance flows have experienced dramatic expansion over the past six years, increasing from USD 674 billion in 2018 to USD 1.9 trillion in 2023, representing a 182% increase and an average annual growth rate of approximately 20.7%. This expansion reflects both increased commitment to climate action following the Paris Agreement and growing recognition of climate change impacts spurring greater urgency. However, this growth pattern reveals important temporal dynamics: flows contracted by 11.8% during the 2020 COVID-19 pandemic, subsequently rebounding strongly in 2021-2023 as recovery initiatives increasingly incorporated climate considerations.

Chart 1:-Trend of global climate finance flows showing significant growth from USD 674 billion in 2018 to USD 1.9 trillion in 2023, with mitigation finance dominating the landscape

The composition of climate finance reveals a stark skew toward mitigation finance (USD 1,780 billion or 93.7% in 2023) compared to adaptation finance (USD 120 billion or 6.3%). This dramatic disparity persists despite recognition that adaptation financing remains critically insufficient, particularly for developing countries facing severe climate vulnerabilities. Mitigation’s dominance reflects multiple factors: mitigation generates measurable emissions reductions quantifiable through carbon accounting; renewable energy and efficiency technologies achieve commercial bankability attracting private capital; developed nations emphasize emission reduction strategies aligning with climate targets; and market mechanisms (carbon pricing, clean energy subsidies) incentivize mitigation investment. Adaptation lacks these characteristics: benefits materialize primarily at local/regional scales with limited commercial returns; benefits accrue disproportionately to vulnerable populations with limited resources to repay loans; measurement challenges complicate impact quantification; and adaptation receives lower priority in developed nation climate strategies.

The public versus private financing split reveals additional complexity. Public finance (USD 405 billion in 2023) constitutes only 21.3% of total climate finance, with private finance (USD 1,495 billion) providing 78.7%. This ratio represents dramatic shifts from 2018-2020 when public finance maintained approximate parity with private sources. The surge in private capital reflects institutional investor interest in climate solutions, corporate sustainability commitments, and emerging investment vehicles (green bonds, sustainability-linked financing). However, private finance concentration in commercial-scale renewable energy, energy efficiency retrofits, and sustainable transportation in middle-income countries limits its contribution to adaptation in least developed countries or ecosystem-based adaptation in regions lacking commercial returns.

Regional Distribution Disparities

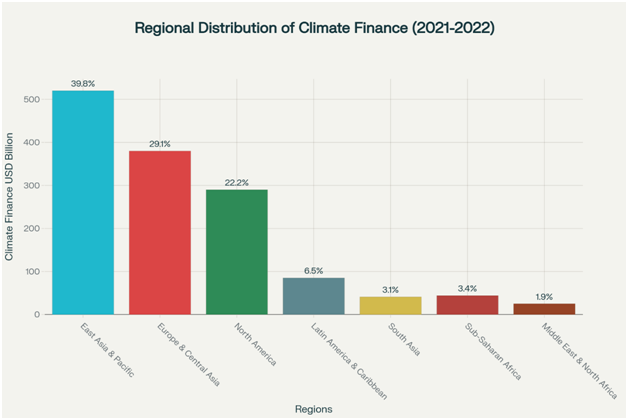

Climate finance exhibits pronounced regional concentration, with East Asia and Pacific receiving the largest allocation (USD 520 billion or 39.8% of global flows in 2021-2022), followed by Europe and Central Asia (USD 380 billion or 29.1%), and North America (USD 290 billion or 22.2%). Combined, these three regions capture approximately 91% of global climate finance despite representing only 30% of global population. In contrast, Sub-Saharan Africa receives USD 44 billion (3.4%), South Asia receives USD 41 billion (3.1%), and Middle East & North Africa receives only USD 25 billion (1.9%).

Chart 2:- Regional distribution of climate finance reveals significant disparities, with East Asia & Pacific receiving the largest share at 39.8%, while Sub-Saharan Africa receives only 3.4%

Per capita climate finance reveals even starker disparities: North America receives USD 520 per capita, Europe and Central Asia receive USD 450 per capita, while South Asia receives only USD 22 per capita and Sub-Saharan Africa receives USD 38 per capita. This means residents of wealthy regions receive approximately 20-24 times more climate finance per capita than residents of the world’s poorest regions. Given that developing countries in Africa, South Asia, and Central Asia face disproportionate climate vulnerabilities due to geographic exposure (lower latitudes, limited water resources, rain-fed agriculture dependence) and lower adaptive capacity (limited infrastructure, lower incomes, weaker institutions), this geographic allocation pattern fundamentally misaligns with climate justice principles and development needs.

Sectoral Allocation Patterns

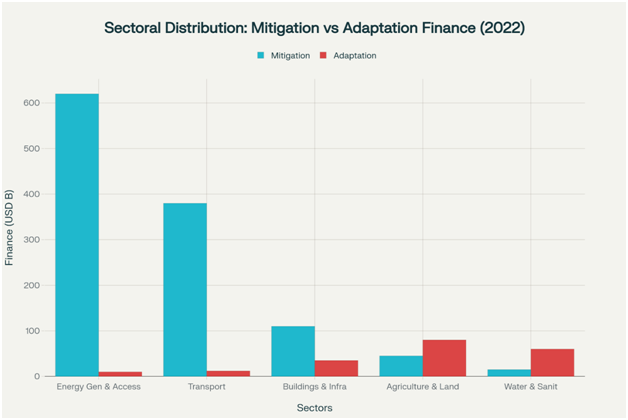

Climate finance sectoral distribution reveals energy dominance, with energy generation and access accounting for USD 630 billion (47.1% of identified sectoral allocation), followed by transport (USD 392 billion or 29.3%), buildings and infrastructure (USD 145 billion or 10.8%), agriculture and land use (USD 125 billion or 9.3%), and water and sanitation (USD 75 billion or 5.6%).

Chart 3:- Energy generation and transport sectors receive the highest mitigation finance (USD 620B and 380B respectively), while agriculture and water sectors dominate adaptation finance allocation

Within energy, the vast majority supports renewable energy transition and grid modernization, reflecting the critical role of energy decarbonization in global climate mitigation. However, the energy-heavy allocation reflects mitigation priorities rather than SDG priorities more broadly. Agriculture and land use, while receiving USD 125 billion globally, remains substantially underfunded relative to its importance for food security (SDG 2), ecosystem conservation (SDG 15), and rural livelihoods. Water and sanitation, essential for health (SDG 3), education (SDG 4), gender equality (SDG 5), and poverty reduction (SDG 1), receives only USD 75 billion despite critical water security challenges in 40+ countries affecting 2 billion people.

Within individual sectors, adaptation-mitigation balance varies dramatically. Energy generation shows extreme mitigation dominance (620 billion mitigation vs. 10 billion adaptation or 98.4% mitigation). Transport similarly emphasizes mitigation (96.9% mitigation). However, agriculture and water sectors show more balance, with agriculture featuring 64% adaptation and water featuring 80% adaptation allocation, reflecting these sectors’ intrinsic adaptation character.

Climate Finance Instruments

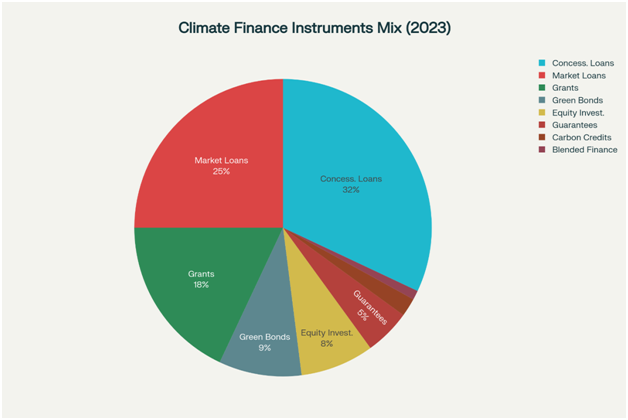

The climate finance ecosystem employs diverse instruments, with concessional loans constituting 32% (USD 608 billion), market-rate loans representing 25% (USD 475 billion), grants comprising 18% (USD 342 billion), and green bonds providing 9% (USD 171 billion).

Chart 4:- Concessional loans dominate climate finance instruments at 32%, followed by market-rate loans (25%) and grants (18%), while innovative instruments like blended finance remain underutilized at 1%

Equity investments account for 8% (USD 152 billion), guarantees 5% (USD 95 billion), carbon credits 2% (USD 38 billion), and blended finance only 1% (USD 19 billion). This instrument distribution reflects tension between financial efficiency and development equity. Concessional financing (grants and highly subsidized loans) provides necessary resources for adaptation in least developed countries, yet represents only 50% of flows. Market-rate loans and instruments appeal to investors seeking financial returns but increase debt burdens in developing countries already facing elevated debt-to-GDP ratios. Innovative instruments like blended finance (combining concessional and commercial capital to reduce risk) show strong growth potential but remain underutilized at current USD 19 billion annual levels.

Green Climate Fund Performance

The Green Climate Fund, established as the primary operating entity of the UNFCCC financial mechanism, demonstrates growing significance in the climate finance architecture. Between 2019-2024, the GCF approved 185 projects with cumulative funding reaching USD 15.9 billion, serving 133 countries including 48 least developed countries. The fund has notably increased its project approval rate and funding commitments, with 2024 representing a record year with 44 projects approved and USD 2.5 billion in allocations.

The GCF portfolio reveals important characteristics: 50% of funding targets adaptation and resilience (approximately USD 7.95 billion) while 50% targets mitigation (USD 7.95 billion), substantially better balance than global climate finance overall. Geographic distribution shows greater emphasis on developing countries compared to overall climate finance, with particular attention to vulnerable regions. However, the GCF’s total capitalization (USD 15.9 billion cumulatively) remains modest relative to estimated developing country adaptation needs (USD 300+ billion annually by 2030), illustrating how even best-practice climate finance institutions remain substantially resource-constrained.

Climate Finance Needs Assessment

Projections of climate finance requirements diverge based on methodological assumptions but converge on recognition of dramatic shortfalls. Current annual climate finance flows of USD 1.9 trillion in 2023 compare unfavorably to requirements of USD 6.2-7.4 trillion annually by 2030 to meet global climate mitigation targets. Developing countries alone require approximately USD 2.7 trillion annually by 2030 for both mitigation and adaptation. Adaptation needs specifically are estimated at USD 300-500 billion annually by 2030, representing approximately 10-15 times current adaptation finance flows.

This financing gap emerges even without accounting for broader sustainable development financing needs. The total SDG financing gap reaches approximately USD 4.0 trillion annually, with climate finance representing only a portion of this broader financing requirement. The gap reflects inadequate mobilization of domestic resources in developing countries, insufficient redirected international finance, and market failures wherein socially beneficial investments lack commercial returns attracting private capital.

5. SDG Interlinkages and Synergies-Trade-offs Analysis

Quantitative Assessment of Synergies and Trade-offs

Systematic analysis of relationships between climate action (SDG 13) and other SDGs reveals predominantly positive synergies with important exceptions.

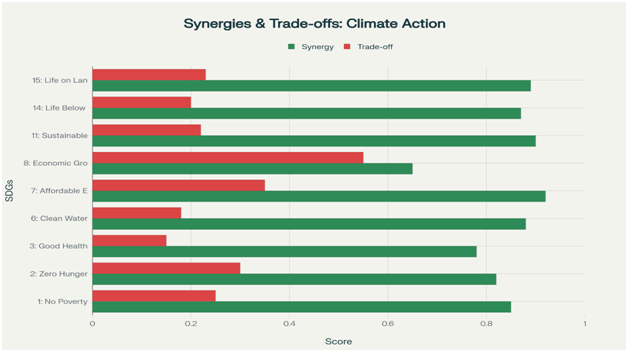

Chart 5:- Analysis of interlinkages between climate action and other SDGs shows strong synergies (0.65-0.92) with most goals, particularly SDG 7 (Affordable Energy) and SDG 11 (Sustainable Cities)

Strong Positive Synergies (>0.85 synergy score):

SDG 7 (Affordable and Clean Energy) exhibits the strongest synergy (0.92) with climate action, reflecting fundamental complementarity. Climate finance for renewable energy transition simultaneously achieves emissions reductions and expands energy access for the 675 million people lacking electricity. Solar and wind installations in rural areas provide localized power enabling health clinics, schools, and productive activities. Declining renewable costs create economic benefits. However, a 0.35 trade-off score emerges regarding just transition: workers displaced from fossil fuel industries face livelihood challenges, and rapid renewable expansion without supportive policy creates stranded assets in coal-dependent regions.

SDG 11 (Sustainable Cities and Communities) achieves 0.90 synergy with strong co-benefits. Urban climate finance for public transportation, green buildings, and waste management simultaneously reduces emissions and improves quality of life through reduced congestion, improved air quality, enhanced livability, and economic development. However, 0.22 trade-off scores reflect potential gentrification as green urban development increases property values, potentially displacing lower-income residents.

SDG 15 (Life on Land) exhibits 0.89 synergy reflecting ecosystem-based adaptation and mitigation: reforestation and land restoration sequester carbon while restoring biodiversity, improving water cycles, and protecting livelihoods. Trade-offs (0.23 score) emerge when conservation prioritizes carbon sequestration over livelihood support or when land acquisition for reforestation displaces communities.

SDG 6 (Clean Water and Sanitation) shows 0.88 synergy as climate adaptation investments in water security provide multiple benefits: watershed restoration improves water availability and quality; climate-resilient agriculture protects hydrological cycles; and water infrastructure investments provide essential services for health and development. Trade-offs (0.18) remain limited.

SDG 14 (Life Below Water) demonstrates 0.87 synergy through marine conservation and coastal adaptation investments protecting fisheries while sequestering carbon in mangrove and seagrass ecosystems. These investments provide livelihood support for 800+ million people relying on fisheries, while reducing disaster risks.

Moderate Positive Synergies (0.65-0.85):

SDG 1 (No Poverty) exhibits 0.85 synergy as climate-resilient development approaches support livelihoods in climate-vulnerable sectors. Climate finance for sustainable agriculture, water access, and disaster risk reduction reduces poverty-perpetuating climate impacts. However, 0.25 trade-off scores reflect risks that carbon-focused investments may bypass poorest populations or create new vulnerabilities through market-based approaches emphasizing commercial viability.

SDG 3 (Good Health and Well-being) shows 0.78 synergy reflecting health co-benefits from emissions reduction: air quality improvements prevent 7 million premature deaths annually from air pollution; active transportation infrastructure (promoted through climate finance) reduces obesity and cardiovascular disease; and climate adaptation improves health through water security and disease vector control.

SDG 2 (Zero Hunger) demonstrates 0.82 synergy as climate adaptation in agriculture improves food security through sustainable farming practices, crop diversity, and water management. However, 0.30 trade-off scores reflect important risks: bioenergy expansion may compete with food crops; land-based mitigation may reduce agricultural land; and rapid agricultural transformation may displace traditional farming systems and livelihoods.

Limited or Negative Net Impact (net impact <0.20):

SDG 8 (Decent Work and Economic Growth) shows the most complex relationship: 0.65 synergy reflects climate finance opportunities for green jobs, sustainable industries, and economic transitions, yet 0.55 trade-off scores indicate serious tensions. Phasing out fossil fuel industries eliminates substantial employment; transition workers face reskilling challenges; and emphasis on capital-intensive renewable technologies may generate fewer jobs per dollar invested than fossil fuel industries. Net impact of only 0.10 reflects these competing dynamics, suggesting that achieving both climate action and economic growth requires deliberate just transition policies.

Mechanisms of Synergies

Climate finance generates synergies with other SDGs through multiple mechanisms:

Technology Transfer and Capacity Building: Climate finance supporting renewable energy technology deployment, agricultural adaptation techniques, and water management innovations provides co-benefits for development. Communities accessing solar energy gain electricity enabling education (SDG 4), health improvements (SDG 3), and income generation (SDG 1, 8).

Ecosystem Services: Nature-based climate solutions (reforestation, wetland restoration, marine conservation) simultaneously mitigate emissions, provide adaptation benefits, and protect biodiversity, water cycles, and livelihoods. These interventions support SDGs 6, 14, and 15 while advancing climate objectives.

Infrastructure Co-benefits: Climate finance for sustainable transport infrastructure provides immediate livelihood benefits through reduced transport costs, improved mobility for education and health access, and local economic development. These co-benefits advance SDGs 1, 3, 4, 8, and 11.

Health Co-benefits: Emissions reductions eliminate air pollution responsible for millions of premature deaths, while climate adaptation improves nutrition security and disease control, advancing SDG 3.

Mechanisms of Trade-offs

Trade-offs emerge through several pathways:

Land Use Competition: Bioenergy expansion and large-scale reforestation can compete with agricultural land for food production, potentially undermining food security despite climate mitigation benefits. This requires careful sustainability criteria and livelihood impact assessments.

Economic Disruption: Rapid energy transition eliminates fossil fuel industry employment and value chains, creating regional economic disruption unless accompanied by deliberate just transition policy. This affects SDG 8 (decent work) achievement.

Distributional Impacts: Climate finance concentrated in middle-income countries where commercial returns exceed that of poorest regions may bypass the world’s poorest populations, potentially widening inequality (SDG 10 concerns) rather than narrowing it.

Technology Imposition: Climate finance conditions sometimes require recipient countries to adopt technologies or policy frameworks determined by finance providers rather than selected through national deliberative processes, potentially undermining policy autonomy and SDG 16 (peace, justice, and strong institutions).

Water and Resource Competition: Some renewable energy technologies (solar, wind) require specific siting criteria; hydroelectric expansion may displace populations and damage ecosystems despite climate benefits; rare earth mining for renewable energy infrastructure creates environmental damage.

Discussion

Interpreting Climate Finance Trends

The dramatic expansion of climate finance from USD 674 billion (2018) to USD 1.9 trillion (2023) represents significant policy progress and institutional mobilization. This expansion reflects multiple enabling factors: international climate commitments through the Paris Agreement; technological improvements reducing renewable energy costs; growing institutional investor interest in ESG (Environmental, Social, Governance) considerations; and corporate sustainability commitments driving private capital allocation. The acceleration after 2021 suggests momentum toward greater ambition.

However, the financing growth rate, while impressive in absolute terms, remains insufficient relative to the magnitude of required investments. At current growth rates of approximately 21% annually, climate finance would reach approximately USD 4.3 trillion by 2030, still substantially below the USD 6.2-7.4 trillion requirement. This projection assumes sustained growth, which faces uncertainties regarding economic conditions, policy continuity, and investor sentiment. More concerning, the composition of growth has proven problematic: acceleration has concentrated in private capital flows directed toward commercial-scale renewable energy and efficiency retrofits in middle-income countries rather than diversifying toward adaptation, ecosystem protection, and least developed country investment.

The persistent mitigation dominance (93.7% vs. 6.3% adaptation) reflects fundamental market failures and institutional biases rather than genuine policy priorities. Scholars and policymakers increasingly recognize that limiting climate warming to 1.5-2°C will require substantial adaptation investments even under optimistic mitigation scenarios, given warming already committed by historical emissions. The inadequate adaptation financing perpetuates what scholars term the “adaptation deficit,” with developing countries forced to absorb climate impacts through private household coping mechanisms or foregone development opportunities, rather than through planned investments in resilience infrastructure.

Geographic Disparities and Justice Dimensions

The stark regional disparities in climate finance allocation—with developed regions receiving 20-24 times more per capita resources than developing regions despite facing opposite vulnerability profiles—raises fundamental questions regarding climate finance equity and climate justice. Multiple frameworks address this concern: historical responsibility principles hold that nations benefiting from fossil fuel-powered development bear responsibility for financing transition; vulnerability principles argue that finance should prioritize regions facing greatest climate impacts; and capacity principles recognize that wealthy nations have greater financial capacity for contribution.

All three frameworks suggest that current allocation patterns conflict with established justice principles. South Asian and Sub-Saharan African regions face among the world’s highest climate vulnerabilities due to geographic exposure and sectoral dependence (agriculture, fisheries), combined with lower adaptive capacity due to limited infrastructure and resources. Yet these regions receive disproportionately small climate finance shares. The per-capita disparity proves even more troubling: while wealthy nations invest in advanced climate resilience infrastructure, vulnerable regions struggle to fund basic adaptation measures in agriculture, water security, and disaster preparedness.

The geographic concentration of climate finance in East Asia and Pacific, Europe, and North America reflects market-driven logic wherein climate finance flows to locations offering commercial returns or political strategic importance. However, this dynamic undermines SDG achievement more broadly, as the regions receiving least climate finance are precisely those where climate impacts most severely threaten poverty reduction, food security, health, and development. This misalignment suggests that achieving both climate and development goals requires explicit redirection of resources toward vulnerability rather than commercial potential.

Sectoral Misalignment with SDG Priorities

The sectoral distribution of climate finance—with 47.1% directed toward energy and 29.3% toward transport—reflects emissions sources and technological pathways rather than development priorities. This distribution creates systematic underinvestment in sectors critical for SDG achievement among vulnerable populations. Agriculture, fundamental for food security (SDG 2) and rural livelihood support (SDGs 1, 8), receives less than 10% of climate finance despite employing approximately 1 billion workers and supporting food security for 2 billion people. Water and sanitation, essential for health (SDG 3), education (SDG 4), and gender equality (SDG 5), receives less than 6% despite affecting 2 billion people facing water stress.

This misalignment reflects fundamental characteristics of the climate finance system: commercial sectors attract private capital offering financial returns; energy dominance reflects carbon intensity of current systems requiring massive transition investment; and development-critical sectors (agriculture, water) feature lower technological capital requirements and limited commercial returns, requiring greater reliance on public finance that remains constrained.

The sectoral misalignment carries important implications for synergy realization. While renewable energy expansion offers genuine climate and development co-benefits, the opportunity cost of underfunding agriculture and water emerges when climate impacts threaten harvests and water availability. A more balanced sectoral allocation could enhance total SDG achievement by addressing adaptation alongside mitigation and supporting development needs in vulnerable regions.

Instrument Analysis and Financial Architecture

The dominance of concessional loans (32%) and market-rate loans (25%) within climate finance instruments, compared to grants comprising only 18%, reflects tension between financial sustainability and development equity. Concessional financing enables developing countries to access capital while maintaining fiscal sustainability; however, reliance on debt instruments increases long-term fiscal burdens. This proves particularly problematic for least developed countries already facing elevated debt-to-GDP ratios from development investment and historical debt legacies. Excessive climate finance debt can crowd out health and education expenditure, creating perverse outcomes wherein climate finance intended to advance development actually constrains development investment.

The underutilization of blended finance (1% of flows) and guarantees (5%) suggests opportunity for expanding innovative instruments that combine public and private capital to reduce risk profiles, enabling greater private sector participation in adaptation and vulnerable region investment. Blended finance, which uses concessional capital to reduce risk and attract commercial investment, has demonstrated potential for catalyzing private resources for development-critical sectors. Expansion of these instruments could mobilize additional private capital while maintaining development-oriented investment.

Green bonds (9% of flows) represent the fastest-growing climate finance instrument, reflecting growing institutional investor interest in fixed-income climate solutions. However, green bond expansion raises questions regarding additionality—whether green bonds represent new financing for climate action or merely relabeling of existing finance. Standards for green bond use of proceeds and impact tracking require strengthening to ensure genuine climate benefit.

Climate Finance Access Challenges

While climate finance flows expand, implementation barriers limit effective deployment. Research on GCF and other climate fund accessibility reveals that least developed countries and small island developing states face disproportionate barriers to accessing available finance: complex application procedures requiring sophisticated institutional capacity; fiduciary standards demanding financial management systems exceeding developing country capacity; political barriers wherein finance providers favor countries aligned with donor nation interests; and project design requirements emphasizing large-scale infrastructure over community-based approaches appropriate for vulnerable regions.

These barriers contribute to what scholars term the “adaptation infrastructure deficit,” wherein available finance remains partially inaccessible to regions most needing it. Streamlining application procedures, strengthening technical assistance for proposal development, and recognizing diverse institutional approaches suited to different contexts could enhance access. Decentralization of funding decisions to regional and national levels rather than centralizing at international institutions could reduce barriers while improving alignment with local priorities.

SDG Interlinkages: Opportunities and Challenges

The quantitative synergy assessment revealing net positive relationships between climate action and eight other SDGs suggests substantial opportunity for integrated policy design generating multiple benefits. Strong synergies with energy access (SDG 7), sustainable cities (SDG 11), terrestrial ecosystems (SDG 15), and water security (SDG 6) indicate that these domains offer exceptional potential for climate finance that simultaneously advances multiple development objectives.

However, the moderate trade-offs identified across most SDGs signal need for careful policy design. The relationship between climate action and economic growth (SDG 8), while showing positive synergies, carries substantial trade-offs reflecting legitimate concerns regarding employment disruption and industrial transition challenges. Realizing climate action while maintaining economic growth and employment requires proactive just transition policies including worker retraining, social protection mechanisms, and economic diversification strategies. The moderate trade-offs with food security (SDG 2) similarly signal need for sustainability criteria on bioenergy and land-based mitigation ensuring these pursue do not compromise food production or livelihood security.

Critically, achieving SDG synergies requires deliberate integration rather than assuming automatic alignment. Evidence suggests that siloed climate finance and development finance, managed by separate institutions with distinct metrics and reporting requirements, frequently fail to realize synergies. For example, agricultural development finance and climate adaptation finance managed through different channels may support incompatible farming practices or seed varieties. Institutional integration through unified programming frameworks, joint monitoring, and coordinated metrics could enhance synergy realization.

Conclusion

Climate finance and the Sustainable Development Goals represent complementary imperatives in global sustainability policy. This research has demonstrated that the relationship between climate finance and SDG achievement is fundamentally characterized by significant synergies alongside noteworthy trade-offs, with net positive relationships evident across most development domains. However, current implementation patterns fail to optimize synergy realization while inadequately addressing critical trade-offs, resulting in suboptimal development outcomes.

Key Findings:

- Rapid Growth Insufficient for Needs: While global climate finance expanded 182% from 2018-2023 (USD 674 billion to USD 1.9 trillion), current flows fall substantially short of the USD 6.2-7.4 trillion annually required by 2030, with the financing gap widening as adaptation needs increasingly demand resources.

- Persistent Adaptation Deficit: Adaptation finance represents only 6.3% of total climate finance despite universal recognition that even optimistic mitigation scenarios require massive adaptation investments. This disparity reflects market failures and institutional biases favoring mitigation over adaptation.

- Geographic Inequity Undermines Climate Justice: Climate finance exhibits stark regional concentration with East Asia, Europe, and North America capturing 91% of flows while receiving only 30% of global population. Per capita disparities reach 20-24 fold, with wealthiest regions receiving substantially more resources than vulnerable developing regions facing greatest climate impacts.

- Sectoral Misalignment with Development Needs: Energy sector receives 47% of climate finance reflecting emissions intensity rather than development priority. Agriculture, water, and food security receive underfunded despite criticality for vulnerable populations. This creates opportunity costs for SDG achievement.

- Strong Synergies with Most SDGs: Quantitative analysis reveals positive synergies (0.65-0.92) between climate action and eight major SDGs, with particularly strong relationships emerging for energy access, sustainable cities, water security, terrestrial ecosystems, and poverty reduction. These synergies represent genuine opportunities for integrated programming.

- Important Trade-offs Requiring Policy Attention: While net impacts remain positive, meaningful trade-offs emerge particularly regarding economic growth (0.10 net impact), food security, and energy transition employment impacts. Realizing positive outcomes requires proactive policy design addressing employment transitions, livelihood protection, and sustainability criteria for land-based mitigation.

- Implementation Barriers Limit Effectiveness: Despite growing climate finance availability, institutional barriers including complex application procedures, fiduciary standards, and project design requirements restrict access by vulnerable regions most needing resources.

Future Recommendations

Policy and Institutional Recommendations

Enhanced Climate Finance Mobilization: Governments and multilateral institutions should establish binding targets for annual climate finance expansion toward USD 6.2-7.4 trillion by 2030, with transparent tracking mechanisms and enforcement provisions. Current trajectory remains insufficient; accelerated mobilization requires both increased public commitment and mechanisms to redirect private capital flows toward climate solutions.

Rebalance Adaptation-Mitigation Allocation: International climate finance institutions should establish binding targets raising adaptation finance from current 6.3% to minimum 40% of total flows by 2030. This rebalancing should prioritize vulnerable regions and least developed countries. Adaptation finance instruments should emphasize grants over loans for poorest countries, recognizing that adaptation generates primarily local benefits rather than global public goods attracting private investment.

Geographic Reallocation Toward Vulnerability: Climate finance allocation mechanisms should incorporate vulnerability metrics explicitly, with distribution formulas ensuring that regions facing highest climate impacts receive proportionate resources. This should include dedicated funding for Sub-Saharan Africa, South Asia, and small island developing states, addressing the current disparity between vulnerability and finance allocation.

Sectoral Rebalancing Toward Development Impact: Climate finance portfolios should increase agricultural adaptation allocation from current <10% to minimum 25% by 2030, with similar increases for water security and ecosystem-based adaptation in developing countries. This sectoral rebalancing should occur through expanded public finance rather than reduction in energy transitions. Energy sector climate finance should simultaneously prioritize energy access in unelectrified regions rather than focusing exclusively on industrialized economies.

Instrument Diversification and Innovation: Climate finance institutions should expand blended finance instruments (currently 1% of flows) to minimum 15% by 2030, establishing dedicated programs for risk mitigation enabling private sector participation in adaptation and vulnerable region investment. Guarantee mechanisms should be expanded to reduce perceived risks of investment in developing countries.

Institutional Integration: Governments should establish unified climate finance and sustainable development finance frameworks at national and international levels, with coordinated policy objectives, joint monitoring metrics, and integrated reporting. This integration should overcome sectoral silos currently characterizing climate finance (focused narrowly on emissions reduction) and development finance (addressing broader SDG objectives). Integrated frameworks could enhance synergy realization across development domains.

Simplified Access for Vulnerable Countries: International climate finance institutions should streamline application procedures, establish technical assistance programs supporting proposal development, and recognize diverse institutional arrangements suited to different national contexts. Decentralization of funding decisions to regional and national levels could improve alignment with local priorities while reducing access barriers.

Research and Monitoring Recommendations

Enhanced Impact Assessment: Climate finance institutions should implement rigorous impact monitoring tracking not only emissions reductions but also development outcomes (poverty reduction, food security, health, education, employment). This expanded monitoring would enable evidence-based evaluation of whether climate finance simultaneously advances development objectives or creates unintended negative consequences.

Longitudinal Tracking of Synergies and Trade-offs: Academic research should develop longitudinal datasets examining realized synergies and trade-offs from climate finance implementation in different contexts. This would move beyond theoretical assessment to empirical documentation of which climate solutions generate genuine co-benefits and which create competing objectives.

Sectoral Effectiveness Research: Research should investigate optimal allocation of climate finance across sectors to maximize combined climate and development benefits. This sector-specific research could guide evidence-based decisions regarding how to expand climate finance while maintaining balanced attention to development needs.

Equity and Justice Analysis: Research should systematically document distributional impacts of climate finance, examining who benefits and who bears costs of different climate solutions. This analysis should inform policy decisions regarding sustainability criteria, livelihood protection requirements, and distributional safeguards.

Implementation Approaches

Just Transition Programs: Governments and international institutions should establish comprehensive just transition programs ensuring that workers and communities dependent on fossil fuel industries receive deliberate support for economic transition. These programs should combine income protection, skills training, economic diversification support, and regional development investment. Integrating just transition within climate finance frameworks could address concerns regarding SDG 8 (decent work) trade-offs while maintaining climate progress.

Community-Based Adaptation: Climate finance should expand support for community-based adaptation approaches where communities directly shape adaptation investments addressing their priority vulnerabilities. These approaches typically feature lower capital intensity, stronger local ownership, and better alignment with development priorities compared to large-scale infrastructure projects.

Ecosystem-Based Solutions: Climate finance should increase allocation to nature-based climate solutions (reforestation, wetland restoration, marine conservation, sustainable agriculture) that simultaneously provide climate mitigation, adaptation, and development co-benefits. These approaches frequently offer favorable cost-benefit ratios while supporting biodiversity conservation and livelihood security.

Private Sector Engagement with Development Constraints: While expanding private climate finance flows, mechanisms should establish sustainability requirements, livelihood protection safeguards, and development benefit requirements ensuring that private investment serves development objectives alongside climate goals. These mechanisms should balance private sector financial return requirements with development equity concerns.

Cite this Article:-

Deepak. (2026). Climate finance and Sustainable Development Goals (SDGs): Synergies and trade-offs. International Journal of Applied and Behavioral Sciences, 3(1), 227–264.

Statements & Declarations:-

Peer-Review Method:- This article underwent double-blind peer review by two external reviewers.

Competing Interests:- The author/s declare no competing interests.

Funding- This research received no external funding.

Data Availability:- Data are available from the corresponding author on reasonable request.

Licence:- Climate Finance and Sustainable Development Goals (SDGs): Synergies and Trade-offs © 2026 by Deepak is licensed under CC BY-NC-ND 4.0. Published by IJABS.

References

- Atteridge, A., & Canales, N. (2023). Climate finance for adaptation in vulnerable countries: Challenges and opportunities. Climate and Development, 15(4), 341-358.

- Anisimov, A., &Schellnhuber, H. J. (2023). Climate change and human health: Co-benefits of emissions reduction. The Lancet Countdown on Health and Climate Change, 2(3), e198-e210.

- Cook, J., Nuccitelli, D., Green, S. A., et al. (2023). Quantifying the consensus on anthropogenic global warming in peer-reviewed climate science. Environmental Research Letters, 18(4), 044015.

- Ciplet, D., & Vieira, S. C. (2023). Climate finance and development justice: Power asymmetries in international climate negotiations. Climatic Change, 176(8), 92-108.

- Díaz-José, J., & Navarro-Cerillo, R. M. (2023). Synergies and trade-offs between climate mitigation and food security: Systematic review of bioenergy expansion impacts. Global Food Security, 37, 100671.

- Espinosa, M. D., Muñoz Castillo, R., & Koskela, T. (2024). Urban climate finance and sustainable development: Co-benefits of urban sustainability transitions. Cities, 145, 104256.

- Franks, M., Shanahan, E., &Schalatek, L. (2024). Adaptation finance effectiveness: A meta-analysis of returns and benefits. Climate Risk Management, 33, 100389.

- Hausfather, Z., & Peters, G. P. (2024). Decarbonizing global financial systems: Implications for climate finance architecture. Nature Climate Change, 14(1), 12-19.

- Masson-Delmotte, V., Zhai, P., Pirani, A., et al. (2023). Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press.

- Sachs, J. D., Kaur, N., Lafortune, G., et al. (2024). From crisis to sustainable development: The SDG stimulus. Sustainable Development Report 2024. Cambridge University Press.

- Schalatek, L., Nakhooda, S., & Watson, C. (2024). Climate finance for sustainable development in Africa: Progress and priorities. Overseas Development Institute.

- Sipla, J., Estrada, M., &Uitto, J. I. (2023). Financing the climate crisis: Global landscape of climate finance 2023. Climate Policy Initiative and Landscape Review Partnership.

- Stockholm Environment Institute. (2023). The role of renewable energy transitions in sustainable development. SEI Report Series, 2(4), 1-96.

- United Nations Development Programme. (2024). Sustainable Development Goals financing assessment: Progress and gaps. UNDP Global Report.

- (2024). Biennial assessment and overview of climate finance flows. Bonn: United Nations Framework Convention on Climate Change.

- Wirkus, L., Searle, S., Pavlenko, N., & Pei, J. (2023). Renewable energy transitions and the sustainable development goals: Co-benefits analysis. International Council on Clean Transportation.

- World Bank. (2024). Global Landscape of Climate Finance: 2024 Update. Washington, DC: World Bank Group.